Cash Discount,

done 100% compliant.

ZeroPoint is the cash-discount compliance expert. Our fully compliant program legally eliminates your credit card processing fees - so you keep 100% of every transaction. Modern hardware, next-day funding, no contracts.

Build your perfect cash-discount compliant Clover system.

Answer a few quick questions and we'll recommend the right Clover hardware and add-ons - sold, set up, and supported locally, on a compliant cash-discount program that keeps 100% of every sale.

What type of business do you run?

Eliminating credit card processing fees is all we do - and we've done it since 2017.

Set up to our compliance checklist - and backed by up to $5,000.

Your setup is designed to align with Visa rules and Louisiana SB 254. Complete our compliance checklist and we stand behind it with our $5,000 Compliance Guarantee.

The ZeroPoint Compliance Guarantee is a limited service warranty providing a refund of ZeroPoint program fees up to $5,000 in the aggregate, subject to eligibility conditions, exclusions, and a claims process. It is not insurance and is not legal advice. See the guarantee.

See exactly what you'll keep.

Traditional processors quietly skim 2–4% off every card sale. With ZeroPoint's compliant cash-discount program you keep all of it. Slide your monthly card volume to see your savings.

Start keeping 100%Estimate only. Actual savings depend on your card mix and your current processing fees.

Zero fees, fully explained.

Watch the quick explainer on how ZeroPoint's compliant cash-discount program eliminates your credit card processing fees.

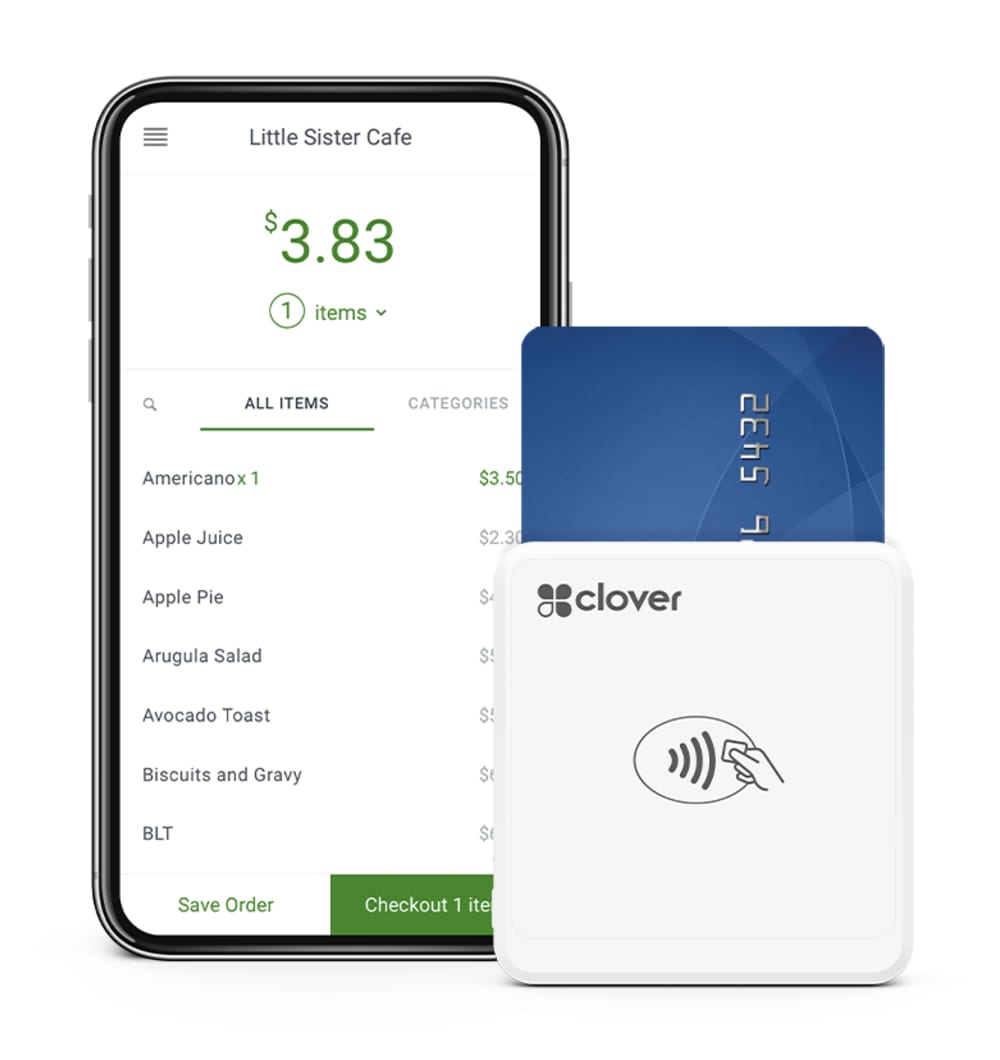

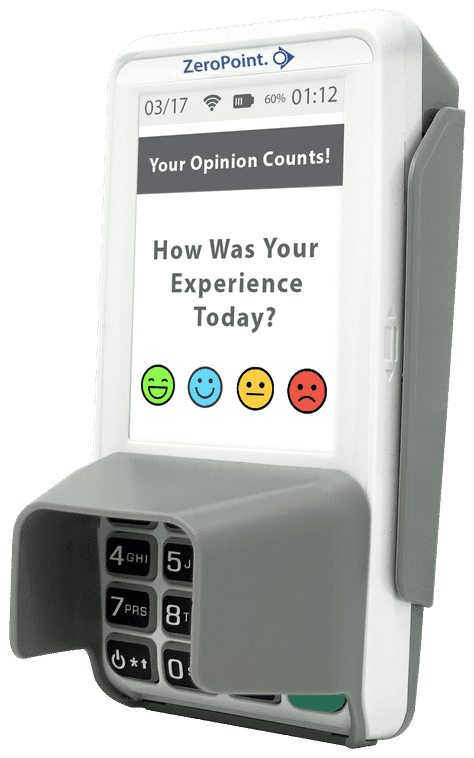

Modern hardware, ready to keep 100%.

Pick the device that fits your counter. Every ZeroPoint terminal runs the compliant cash-discount program out of the box - and we work with nearly every point of sale on the market.

Large touchscreen, contactless, and signature capture with WiFi + Ethernet.

PCI-PTS 5.0 certified, EMV-ready, embedded NFC, and smart tipping.

Pay-at-the-table handheld with bill splitting and 4G + WiFi.

Secure Android handheld with a 5.5" screen for payments anywhere.

Upgrade your payment devices - at no cost.

Switch to ZeroPoint and we'll provide a placement credit card terminal - yours to use free for as long as you process with us.

Plus the full Clover lineup - Mini, Station Solo & Duo, Flex, and Go. One vendor for all your payment needs.

Explore all hardwareThe best way to increase your revenue.

ZeroPoint. credit card processing is a No Fee payment program where a business owner wisely offsets their cost of processing by offering a cash discount to their customers. ZeroPoint is the fastest growing program throughout the country - covering your processing overhead while still maintaining your low prices. The cheapest and best credit card processing solution that will eliminate up to 100% of your credit card processing fees.

More detailsZeroPoint. credit card processing is a Zero Fee program that implements a compliant program that offers customers an option of a cash discount. You Pay Zero credit card processing fees while you will enjoy more cash into your business. All of the cost of credit card processing are offset with our best in the business program. Our Zero-fee processing works on all methods of electronic payments. Visa, MasterCard, American Express, JCB, Voyager, and Wright Express.

Free credit card programs usually use software add-ons to allow your payment gateway, virtual terminal, countertop terminal, or point of sale (POS) system to detect when a credit card is used and automatically offer a Cash Discount to the purchase price. ZeroPoint. Offers our state of the art ZeroPoint Terminal at No Cost to our customers and we work with nearly every Point Of Sale on the market!

Zero-fee processing or “no fee” credit card processing is a processing solution like ZeroPoint. Credit card processing fees are passed to your customers via a Surcharge or Cash Discount automatically. Instead of your business paying the processing costs, you pass those fees along.

With a free credit card processor like ZeroPoint, you can save 100% on processing costs that you would normally pay using a traditional credit card processing option. From hundreds to tens of thousands a month think about what that could do for your business!

Let's get started.

It's never too late to eliminate credit card processing fees. Setup takes ten minutes - you could be processing tomorrow.

1-800-481-5892